A peer-reviewed, multi-clinic study published in the Journal of Assisted Reproduction and Genetics suggests an epigenetic sperm-quality profile can add missing information for infertile couples and clinicians, especially when they are considering IUI (Intrauterine Insemination), IVF (In Vitro Insemination), and/or ICSI (Intracytoplasmic Sperm Injection).

Path Fertility’s review of this capstone research, including the data gathered from preceding studies, confirms clinical data show that “up to 25% of men with a ‘normal’ Semen Analysis result have sperm that are incapable of producing a healthy pregnancy without intervention via advanced fertility techniques.”

SALT LAKE CITY, UT / ACCESS Newswire / March 10, 2026 / A newly published, peer-reviewed study adds real-world evidence that some couples are stuck in “fertility limbo” even after a Semen Analysis comes back “normal.”

According to Andy Olson, CEO and Co-Founder of Path FertilityTM, while it’s obvious that traditional Semen Analysis testing is a crucial first step for understanding sperm viability, for many infertile couples, Semen Analysis alone is not enough.

“This new study reinforces what so many couples experience firsthand: ‘normal’ Semen Analysis test results don’t always come with answers,” Olson said. “In fact, our review of the clinical data shows that up to 25% of men with a ‘normal’ Semen Analysis result have sperm that are incapable of producing a healthy pregnancy without intervention via advanced fertility techniques.

“When couples are stuck in such fertility limbo, they deserve better information sooner. Peer-reviewed, real-world evidence like that shown in this JARG report (and data gathered from prior studies), can help patients and clinicians have a more informed conversation about what to try next and what expectations are realistic.”

PHOTO CAPTION: Andy Olson, CEO and Co-Founder of Path Fertility. March 2026.

What the JARG Study Found

The JARG study analyzed outcomes from 537 couples treated at 10 U.S. fertility clinics and reported a clear pattern: when men had an Abnormal result on an epigenetic sperm test, no pregnancies were recorded from Intrauterine Insemination (IUI) in the outcomes captured in this real-world dataset. {NOTE: Epigenetics is a DNA-level method for scientists to study how cells turn genes on and off, including within sperm cells.}

By contrast, outcomes for in-vitro fertilization (IVF) using Intracytoplasmic Sperm Injection (ICSI) did not show a meaningful difference based on the epigenetic result.

A Quick Translation of the Treatments Mentioned in the Study

To understand why these findings matter, it can help to understand the difference between common fertility treatments. For example,

IUI (intrauterine insemination) is a procedure in which sperm is placed into the uterus around the time of ovulation. It is often tried early by couples attempting to overcome fertility challenges because it is less invasive and less costly than IVF;

IVF (in vitro fertilization) is a process where eggs are retrieved and fertilized in a lab; and

ICSI (intracytoplasmic sperm injection) is a common IVF technique where a highly trained IVF lab embryologist injects a single sperm into an egg to help fertilization occur.

What Semen Analysis Can Show and What it Cannot

Within the medical community, a Semen Analysis test is considered the “Standard of Care” in the field of infertility when it comes to identifying how many sperm are present in a semen sample, how they look, and how they move.

But a Semen Analysis test does not answer the question most infertile couples care about the most: Can these sperm do the job needed to create a pregnancy, especially with a treatment like IUI?

In reality, some sperm can look “normal” with a Semen Analysis test, but still struggle with the key functions required for conception: finding the egg, binding to the egg, penetrating the egg, and fertilizing the egg.

What the Newer Test Looks at, in Plain English

The new JARG study focuses on a still new sperm test based on epigenetics that measures chemical markers that help control how genes behave and how well sperm are likely to function.

SpermQT™, the new sperm-DNA test offered by Path Fertility, is designed to complement Semen Analysis testing by providing this additional epigenetics information about sperm quality and function.

PHOTO CAPTION: The at-home version of SpermQT, a newsperm-DNA test offered by Path Fertility. March 2026

Why this New JARG Study Matters Now

What makes this JARG paper important is that it reports real-world outcomes across 10 clinics, based on anonymous patient data.

Specifically, the JARG study showed that for IUI outcomes, “Abnormal” epigenetic sperm results resulted in zero recorded IUI pregnancies among the couples in the JARG dataset. Conversely, in IVF cases that used ICSI, outcomes did not differ significantly based on the epigenetics result.

For mainstream readers, the takeaway is straightforward: a “normal” Semen Analysis test result is not always the end of the male-fertility conversation.

VIDEO CAPTION: SpermQT introductory video posted on YouTube (https://www.youtube.com/watch?v=EHvFUEBctTs). SpermQT is a new sperm-DNA test offered by Path Fertility.

In fact, additional sperm-focused information may help couples and clinicians set better expectations earlier, especially when deciding whether to keep trying IUI or to move more quickly to more advanced fertility techniques like IVF and/or ICSI.

How Prior Scientific Studies Led to this “Capstone” Result with JARG

This JARG report builds on two peer-reviewed research studies published in 2023, starting with a July 2023 study in Frontiers in Genetics. This data validated the broader scientific approach behind the testing available with SpermQT.

It also found that sperm epigenetic variability was linked with pregnancy and live birth outcomes for IUI, while IVF outcomes did not show a similar separation.

Additionally, a November 2023 study in F&S Science reported that adding epigenetic sperm information could improve how well an analysis of sperm predicted IUI outcomes. This same study reported that IVF outcomes, largely using ICSI, did not show the same differences across epigenetic sperm quality groups.

Together, the 2023 findings laid the scientific groundwork for a greater understanding of sperm viability for infertile couples, while the new JARG paper extended that work into a larger, multi-clinic, real-world setting.

A Perspective from the Clinic

“Many couples hear that the Semen Analysis results are ‘normal’ and assume the male side has been cleared,” said Kaylen Silverberg, MD, Medical Director and fertility specialist with Texas Fertility Center. “However, the type of peer-reviewed research in this JARG study supports a more comprehensive evaluation of male fertility, just as we do with our female patients. SpermQT test results enable couples to make decisions with clearer expectations, especially when considering whether to pursue repeated IUI cycles or proceed to IVF with ICSI.”

A Comment from Path’s Scientific Leadership

“Clinicians and couples alike should think of the data provided by SpermQT results as another piece of the puzzle,” said Kristin Brogaard, Ph.D., Co-Founder and Chief Science Officer of Path Fertility, and a co-author of the JARG study. “Clearly, traditional Semen Analysis testing is still the ‘Standard of Care’ in fertility circles. However, this new test provides a deeper level of detail about sperm function that standard testing does not measure directly, and this additional information can be invaluable to couples struggling with infertility.”

PHOTO CAPTION: Kristin Brogaard, Ph.D., Chief Science Officer and Co-Founder pf Path Fertility. March 2026.

Responsible Interpretation

This new study in JARG reports real-world associations across clinics and treatments, but it does not tell any individual couple what they should do. Patients should discuss testing and treatment options with a qualified clinician who can consider the full medical picture of both partners.

PHOTO CAPTION: SpermQT Test Results Overview Page from Path Fertility. March 2026

About Path Fertility and SpermQT

Path Fertility is focused on raising the “Standard of Care” in male fertility by providing deeper insight into sperm quality and function. As such, SpermQT is a sperm quality test based on epigenetic DNA-markers and is designed to complement Semen Analysis by adding new information related to sperm function.

NOTE: Published Studies Referenced in this Release

SALT LAKE CITY, UT / ACCESS Newswire / March 10, 2026 / Path FertilityTM, an epigenetics-driven fertility technology company, today unveiled the Path Fertility Facts Sheet, a copy of which is embedded below within this news release.

BEGINNING OF THE Path FertilityTM Facts Sheet

Overview

Path FertilityTM helps clinicians and patients uncover male-factor insights that can be missed by “Standard-of-Care” Semen Analysis testing alone, so couples can make more informed fertility treatment decisions sooner.

Path Fertility offers clinically validated testing that evaluates sperm quality and function using epigenetics, providing additional insight into reproductive potential and likely success with common fertility treatment pathways.

Such insights are now validated through three separate, peer-reviewed studies published, respectively, by

The Journal of Assisted Reproduction and Genetics (JARG), 2026;

F&S Science, 2023; and

Frontiers in Genetics, 2023.

Details noted below.

Why this Matters

In fertility care, the male partner is too often “cleared” based on a Semen Analysis result that falls into a reference range. But “Normal” test results do not always mean normal sperm function.

Path Fertility exists to help close that information gap earlier, helping couples reduce avoidable time, cost, and emotional strain.

Flagship Test: SpermQT™

SpermQT™ is a clinically validated epigenetic sperm quality test designed to help predict the likelihood of pregnancy success with certain fertility treatment pathways, especially Intrauterine Insemination (IUI), a procedure where sperm are placed directly into the uterus during ovulation.

VIDEO CAPTION: The “SpermQT vs. Standard Semen Analysis: What’s the Difference?” video from Path Fertility. Video available on YouTube here (https://www.youtube.com/watch?v=nQDm7hngzBk).

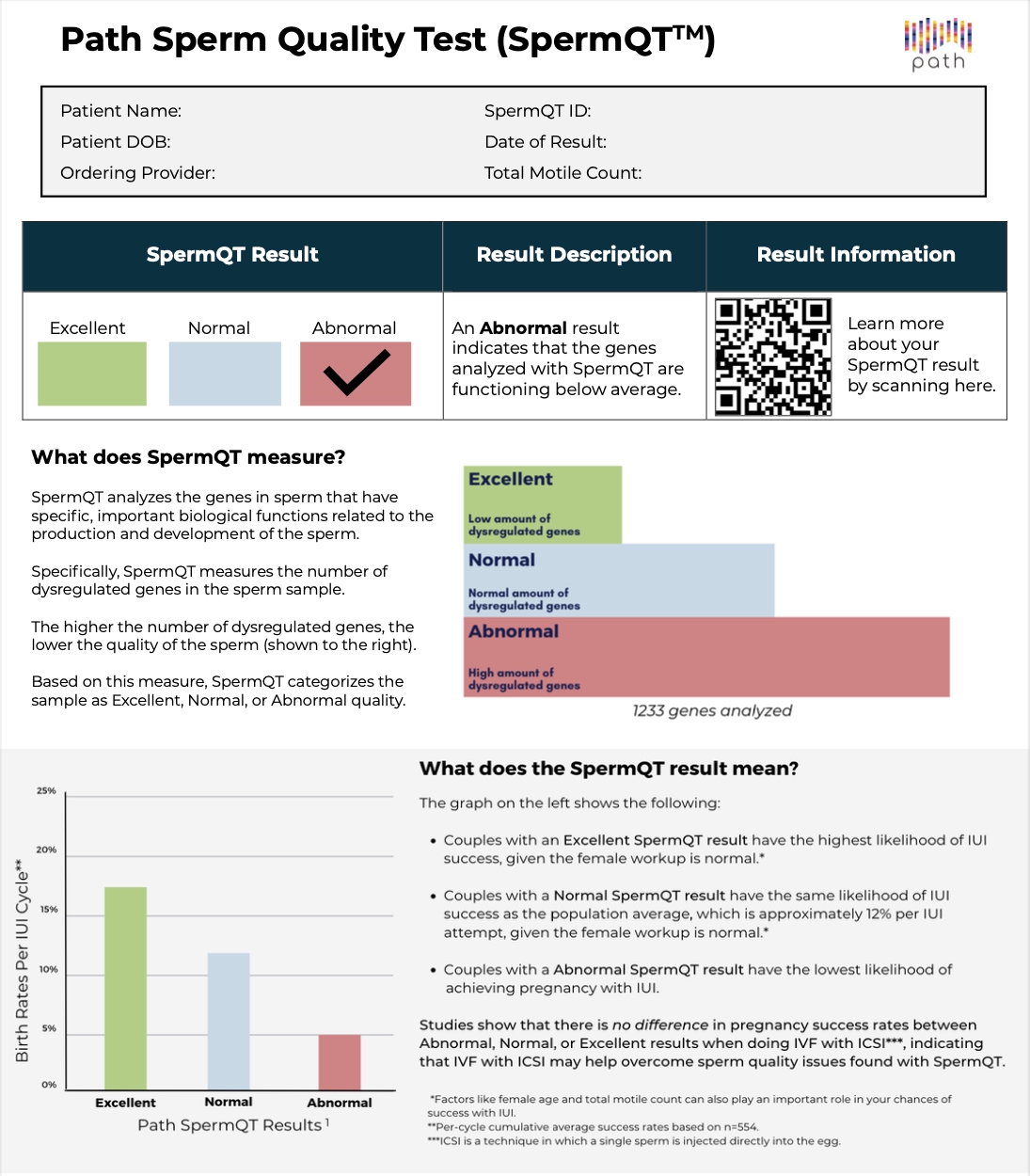

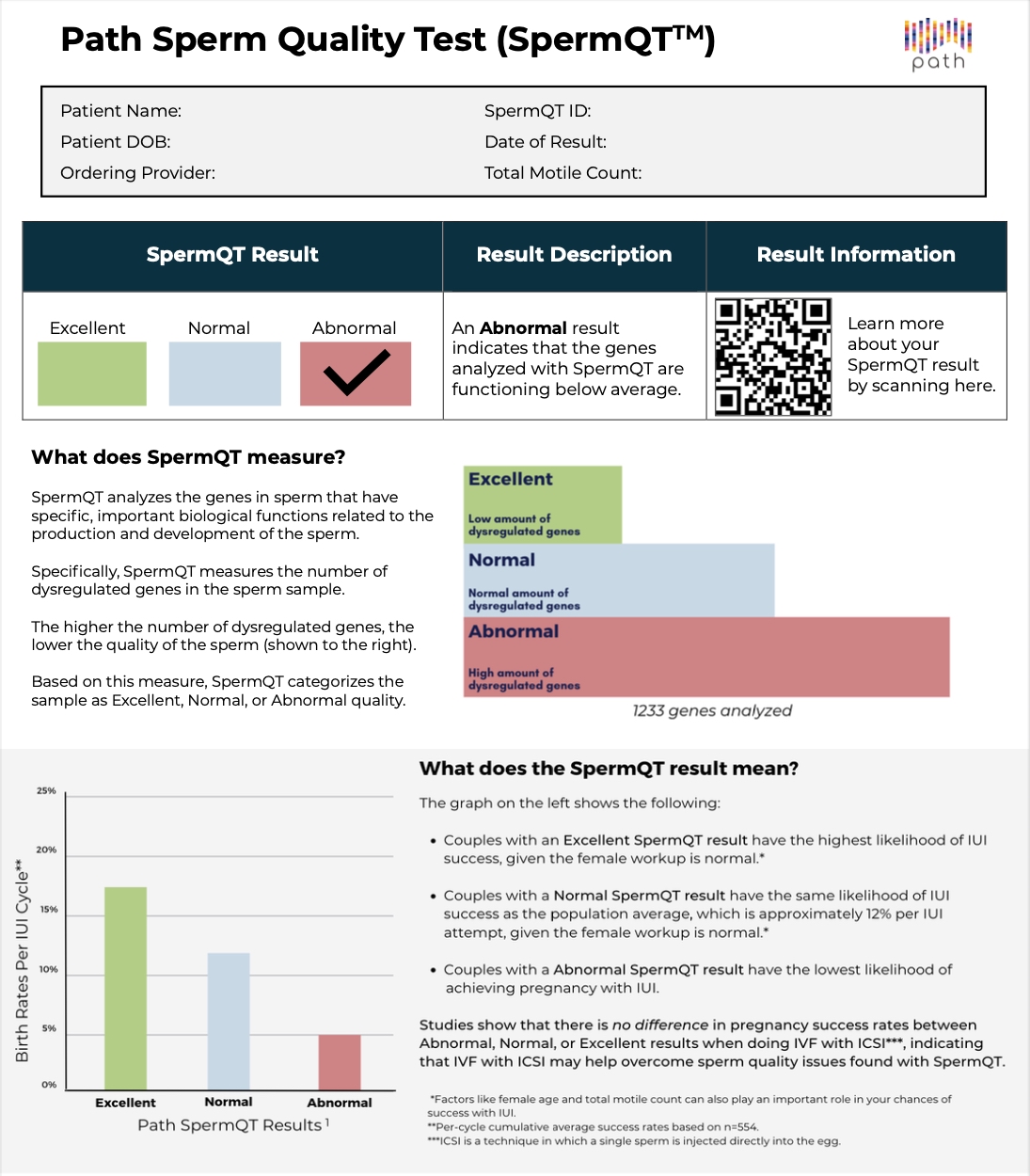

What SpermQT Measures

DNA methylation patterns associated with sperm quality and function, i.e., the presence of certain DNA abnormalities in sperm

Functional capability associated with sperm’s ability to find, bind, penetrate, and fertilize

DNA methylation dysregulation across 1,200+ genes

Results are reported as

Excellent,

Normal, and

Abnormal.

Key Clinical Insights

Review of the clinical data shows that SpermQT results are associated with meaningful differences in pregnancy outcomes for couples pursuing IUI.

SpermQT can identify subfertile men who may be missed by Semen Analysis alone; case in point, 4 out of 5 men with an Abnormal SpermQT result receive a “Normal” test result via Semen Analysis testing.

Either In Vitro Fertilization (IVF), where eggs are fertilized in a lab, or with Intracytoplasmic Sperm Injection (ICSI), where a single sperm is injected into an egg, may help overcome certain sperm quality challenges observed in epigenetic testing.

PHOTO CAPTION: SpermQT overview page from Path Fertility. March 2026

Who can Benefit

Patients / Couples

Couples exploring treatment options and wanting better clarity before choosing a path,

Couples with “unexplained infertility,” including cases with “Normal” Semen Analysis results, and

Couples with failed IUI cycles that need better decision support on next steps.

Providers

Fertility clinics and reproductive endocrinology teams seeking better early male-factor insights,

Urology and andrology practices aiming to improve male workup resolution, and

Clinics seeking stronger prediction support for IUI planning and counseling.

When to use SpermQT

SpermQT is designed as a complement to, and not a replacement of, “Standard-of-Care” Semen Analysis. It is often most useful:

Early in the initial male fertility workup, alongside Semen Analysis,

When Semen Analysis is “Normal” but pregnancy has not occurred as expected, and

After failed IUI attempts to inform whether to continue IUI or move to IVF, with or without ICSI.

How it Works

Physician-ordered test (ordering support available through Path Fertility),

Sample collected via at-home kit (or clinic workflow when applicable),

Testing performed; results returned in about 2 weeks, and

Provider reviews results with the patient to inform next-step planning.

END OF THE Path Fertility Fact Sheet AND COMPLETION OF THE NEWS RELEASE BELOW

About Path Fertility and SpermQT

Path Fertility is focused on raising the “Standard of Care” in male fertility by providing deeper insight into sperm quality and function. As such, SpermQT is a sperm quality test based on epigenetic DNA-markers and is designed to complement Semen Analysis by adding new information related to sperm function.

Path Fertility, SpermQT, and the Path Fertility logos are trademarks of Inherent Biosciences, Inc. All other trademarks are property of their respective owners.

Dr. Raza Bokhari, Executive Chairman & CEO will participate in panel discussions and highlight Company’s AI-enabled Drug Development Strategy

PHILADELPHIA, PA / ACCESS Newswire / March 10, 2026 / Medicus Pharma Ltd. (NASDAQ:MDCX) (“Medicus” or the “Company”), a biotech/life sciences company focused on advancing the clinical development programs of novel and potentially disruptive therapeutics assets, is pleased to announce its participation in the Longwood Miami CEO forum being held March 11-13, 2026, at the Ritz-Carlton Key Biscayne.

Dr. Raza Bokhari, Executive Chairman & CEO of Medicus, will serve on a panel titled “Accelerating the Path to Patient Care” and will highlight company’s AI enabled Drug development strategy designed to make clinical trials not only cost efficient but also time efficient.

Other panelists include Lindsay Edwards, CTO & President of Platform, Relation Therapeutics; Julie Gerberding, CEO, Foundation for the NIH and Former Director, CDC; and Gilmore O’Neill, CEO, Editas Medicine. The panel will be moderated by Jon Cohen, Head of Life Sciences Go-To-Market at ServiceNow.

Longwood Miami CEO is an invitation-only event, that brings together Industry leaders, innovators, thought leaders and opinion makers, who will speak on curated fireside chats, roundtables, and discussion panels.

Notable Participants in the conference include Brent Saunders (CEO, Bausch + Lomb), Chris Boshoff (CSO & President, R&D, Pfizer), Rob Califf (former Commissioner, FDA), Sidney Taurel (Chair Emeritus, Lilly), Bill Mezzanotte (Head, R&D, CSL), David Redfern (President, Corporate Development, GSK), Pablo Cagnoni (Head, R&D, Incyte), Julie Gerberding (former Director, CDC), Bill Hait (Chief Scientific Advisor, AACR; former CMO, J&J), Jeremy Levin (Chair & CEO, Ovid Therapeutics), David Meek (former CEO, Ipsen; CEO, Genetix), Frank Nestle (CEO, Deerfield Discovery), Benj Garrett (Managing Director, Stifel), among others.

Medicus Pharma Ltd. (Nasdaq:MDCX) is a precision-guided biotech/life sciences company focused on accelerating the clinical development programs of novel and potentially disruptive therapeutics assets. The Company is actively engaged in multiple countries across three continents.

SkinJect Inc., a wholly owned subsidiary of Medicus Pharma Ltd., is a development-stage life sciences company focused on commercializing a novel, non-invasive treatment for basal cell skin cancer using a patented dissolvable microneedle patch to deliver a chemotherapeutic agent to eradicate tumor cells.

In August 2025, the Company announced its entry into a non-binding memorandum of understanding (MoU) with Helix Nanotechnologies, Inc. (HelixNano), a Boston-based biotech company focused on developing a proprietary advanced mRNA platform, in respect of their shared mutual interest in the development or commercial arrangement contemplated by the MoU. The MoU is non-binding and shall not be construed to obligate either party to proceed with a joint venture or any further development or commercial arrangement, unless and until definitive agreements are executed.

In August 2025, the Company completed the acquisition of Antev, a UK-based late clinical stage biotech company, developing Teverelix, a next-generation gonadotrophin-releasing hormone (GnRH) antagonist, as a first-in-market product for cardiovascular high-risk advanced prostate cancer patients and patients with first acute urinary retention relapse (AURr) episodes due to enlarged prostate.

Unlike GnRH agonists, which can cause an initial surge in testosterone levels, Teverelix directly suppresses sex hormone production without this surge, potentially reducing cardiovascular risks. This mechanism is particularly beneficial for patients with existing cardiovascular conditions. Teverelix is formulated as a microcrystalline suspension, allowing for sustained release and a six-week dosing interval, which may improve patient compliance and outcomes.

In October 2025, the Company announced a strategic collaboration with the Gorlin Syndrome Alliance (GSA) to advance compassionate access to SkinJect for patients suffering from Gorlin Syndrome, also known as nevoid basal cell carcinoma syndrome.

Under the collaboration, Medicus and the GSA will jointly pursue the Expanded Access IND Program with the FDA to allow patients with multiple, recurrent, or inoperable basal cell carcinomas (BCCs) to access SkinJect under physician-supervised treatment protocols. The initiative aims to establish a framework for expanded access while collecting valuable real-world safety and tolerability data to inform future regulatory filings. It will also more tightly integrate patient community-led insights and data into the design, monitoring, and long-term development of SkinJect in this rare disease population.

In November 2025, the Company received full regulatory and ethical approvals in the United Kingdom to expand its ongoing Phase 2 clinical study (SKNJCT-003) evaluating D-MNA to non-invasively treat BCC of the skin. The approvals were issued by the Medicines and Healthcare products Regulatory Agency (MHRA), the Health Research Authority (HRA) and the Wales Research Ethics Committee (WREC). The MHRA approval followed a comprehensive scientific review of the Investigational Medicinal Product Dossier (IMPD) and protocol. The WREC issued a favorable ethical opinion, and the HRA granted study-wide governance approval, confirming compliance with UK Good Clinical Practice and National Health Service capacity and capability standards.

In December 2025, the Company announced that it has successfully completed enrolment of 90 patients in the United States for Phase 2 clinical study (SKNJCT-003) evaluating D-MNA to non-invasively treat BCC of the skin. The Company expects to secure an end-of-Phase 2 meeting with the FDA in the first half of 2026.

In December 2025, Medicus announced a non-binding letter of intent with Reliant AI Inc., a decision-intelligence company specializing in generative AI for the life sciences industry, to collaborate on the development of an AI-driven clinical data analytics platform. Subject to execution of definitive agreements, the platform is expected to support capital-efficient clinical development through data-driven dynamic clinical-site selection, patient stratification and enrollment forecasting. The initial phase of the collaboration is expected to support an upcoming Teverelix clinical study planned for 2026, with potential expansion into later-stage development programs in collaboration with a strategic partner.

In February 2026, the Company announced that it has received “study may proceed” clearance from the U.S. Food and Drug Administration (FDA) to initiate its Phase 2b dose-optimization study of Teverelix®, an investigational next generation long-acting GnRH antagonist, in men with advanced prostate cancer (APC).

Cautionary Notice on Forward-Looking Statements

Certain information in this news release constitutes “forward-looking information” under applicable securities laws. “Forward-looking information” is defined as disclosure regarding possible events, conditions or financial performance that is based on assumptions about future economic conditions and courses of action and includes, without limitation, statements regarding the Company’s leadership and prospects, the collaboration with GSA including the potential benefits thereof for GSA, those suffering with Gorlin Syndrome and Medicus (including as it relates to the development of SkinJect™), ability to be approved for the Expanded Access IND Program to enable those suffering with Gorlin Syndrome to access SkinJect™ under physician-supervised treatment protocols, the development of Teverelix and expectations concerning, and future outcomes relating to, the development, advancement and commercialization of Teverelix for AURr, high CV risk prostate cancer, women’s health indications like endometriosis, and the potential market opportunities related thereto, the MOU, including the potential signing of definitive agreements between Medicus and HelixNano and the development of thermostable infectious diseases vaccines by combining HelixNano’s proprietary mRNA vaccine platform with Medicus’s proprietary microneedle array (MNA) delivery platform, the Company’s aim to fast-track the clinical development program and convert the SKNJCT-003 exploratory clinical trial into a pivotal clinical trial, and approval from the FDA and the timing thereof, including with respect to the Company’s submission for approval in the FDA Commissioner’s National Priority Voucher program, plans and expectations concerning, and future outcomes relating to, the development, advancement and commercialization of SkinJect through SKNJCT-003 and SKNJCT-004, and the potential market opportunities related thereto, the Company’s expectations regarding reported efficacy findings and whether there will be material changes to its reported SKNJCT-003 topline results and to secure an EOP2 meeting with the FDA in the first half of 2026, entry into definitive documents with Reliant and the expected terms thereof, engaging in proposed Medicus-sponsored studies currently contemplated in the Reliant non-binding letter of intent and the expected benefits thereof, the expansion of SKNJCT-003 into the United Kingdom and the potential benefits therefrom, the advancement of the SKNJCT-004 study and the potential results of and benefits of such study. Forward-looking statements are often but not always, identified by the use of such terms as “may”, “on track”, “aim”, “might”, “will”, “will likely result”, “could,” “designed,” “would”, “should”, “estimate”, “plan”, “project”, “forecast”, “intend”, “expect”, “anticipate”, “believe”, “seek”, “continue”, “target”, “potential” or the negative and/or inverse of such terms or other similar expressions. These statements involve known and unknown risks, uncertainties and other factors, which may cause actual results, performance or achievements to differ materially from those expressed or implied by such statements, including those risk factors described in the Company’s annual report on form 10-K for the year ended December 31, 2024 (the “Annual Report”), and in the Company’s other public filings on EDGAR and SEDAR+, which may impact, among other things, the trading price and liquidity of the Company’s common shares. Forward-looking statements contained in this news release are expressly qualified by this cautionary statement and reflect our expectations as of the date hereof and thus are subject to change thereafter. The Company disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. Readers are further cautioned not to place undue reliance on forward-looking statements as there can be no assurance that the plans, intentions or expectations upon which they are placed will occur. Such information, although considered reasonable by management at the time of preparation, may prove to be incorrect and actual results may differ materially from those anticipated.

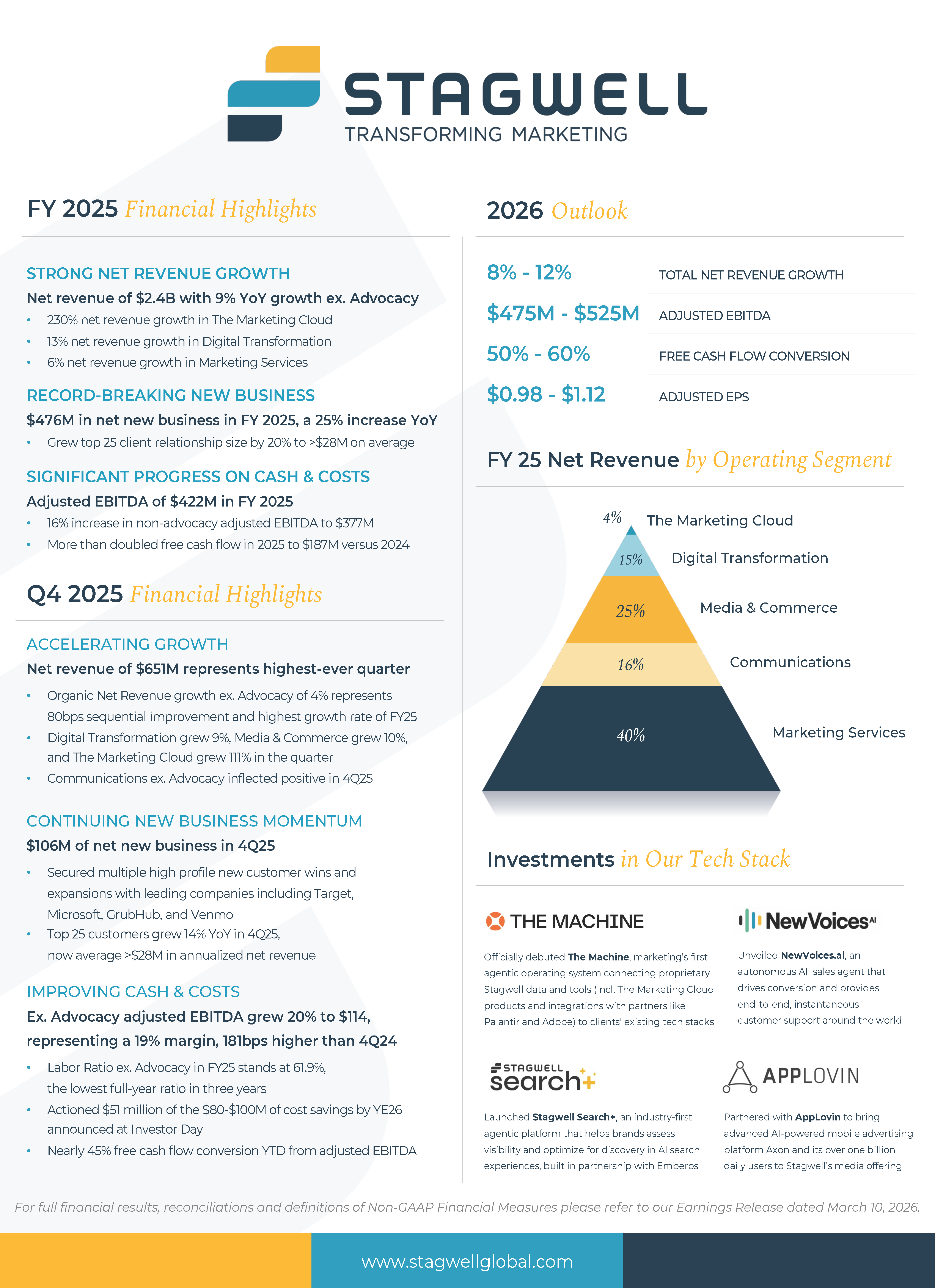

FY25 EPS of $0.08; FY25 Adjusted EPS growth of 5% to $0.83

YoY Increase in Cash Flow from Operations of $148 million; Free Cash Flow more than doubled to $187 million

FY25 YoY Revenue Growth of 2%; FY25 YoY Net Revenue Growth of 6%

FY25 YoY Net Revenue Growth excluding Advocacy of 9%, Digital Transformation Net Revenue Growth of 13%, Marketing Services Net Revenue Growth of 6%

The Marketing Cloud delivered YoY Net Revenue Growth of 230%

FY25 Net Income Attributable to Stagwell Inc. Common Shareholders of $29 million; FY25 Adjusted EBITDA of $422 million; FY25 Adjusted EBITDA ex. Advocacy YoY Growth of 16% to $377 million

Net New Business of $106 million in Q4; LTM Net New Business of $476 million

Company Announces $350 Million Increase in Stock Repurchase Program; $400 Million Now Available Under the Program

Guidance for 2026 of Total Net Revenue Growth of 8% to 12%; Adjusted EBITDA of $475 million to $525 million; Free Cash Flow Conversion of 50% to 60%

NEW YORK CITY, NY / ACCESS Newswire / March 10, 2026 / (NASDAQ:STGW) – Stagwell Inc. (“Stagwell”) today announced financial results for the year ended December 31, 2025.

FOURTH QUARTER AND FULL YEAR RESULTS:

Q4 Revenue of $807 million, an increase of 2% versus the prior year period; FY25 Revenue of $2,909 million, an increase of 2% versus the prior year period;

Q4 Revenue ex. Advocacy of $742 million, an increase of 12% versus the prior year period; FY25 Revenue ex. Advocacy of $2,689 million, an increase of 9% versus the prior year period;

Q4 Net Revenue of $651 million, an increase of 3% versus the prior year period; FY25 Net Revenue of $2,428 million, an increase of 6% versus the prior year period;

Q4 Net Revenue ex. Advocacy of $609 million, an increase of 8% versus the prior year period; FY25 Net Revenue ex. Advocacy of $2,282 million, an increase of 9% versus the prior year period;

Q4 Net Income attributable to Stagwell Inc. Common Shareholders of $13 million versus $3 million in the prior year period; FY25 Net Income attributable to Stagwell Inc. Common Shareholders of $29 million versus $2 million in the prior year period;

Q4 Adjusted EBITDA of $129 million, an increase of 3% versus the prior year period; FY25 Adjusted EBITDA of $422 million, an increase of 1% versus the prior year period;

Q4 Adjusted EBITDA Margin of 20% on net revenue; FY25 Adjusted EBITDA Margin of 17% on net revenue;

Q4 Earnings Per Share Attributable to Stagwell Inc. Common Shareholders of $0.05 versus $0.03 in the prior year period; FY25 Earnings Per Share Attributable to Stagwell Inc. Common Shareholders of $0.08 versus $0.02 in the prior year period;

Q4 Adjusted Earnings Per Share attributable to Stagwell Inc. Common Shareholders of $0.30 versus $0.25 in the prior year period; FY25 Adjusted Earnings Per Share attributable to Stagwell Inc. Common Shareholders of $0.83 versus $0.79 in the prior year period;

YTD Net Cash provided by Operating Activities of $291 million versus $143 million in the prior year period;

Net new business of $106 million in the fourth quarter, last twelve-month net new business of $476 million

See “Non-GAAP Financial Measures” below for explanations and reconciliations of the Company’s non-GAAP financial measures.

“In 2025, Stagwell increased its strategic pivot toward AI applications and services, building a powerful foundation for 2026. With accelerating growth ex-advocacy, record net new business, expanding margins and doubled free cash flow, our FY25 results prove our strategy is working,” shared Mark Penn, Stagwell’s Chairman and CEO. “We see great opportunity in 2026 to capitalize on an industry distracted by restructurings and mergers, and bolster our position as a winner in the age of AI.”

Ryan Greene, Chief Financial Officer, commented: “2025 marked an inflection year for Stagwell, with clear momentum in the underlying business and improving efficiency contributing to strong year-over-year net revenue, adjusted EBITDA and adjusted EPS growth. Proactive cash management meant we more than doubled our free cash flow in 2025. We expect another strong year in 2026, and will be aggressive in our capital allocation to drive shareholder value.”

Financial Outlook

2026 financial guidance is as follows:

Total Net Revenue growth of 8% to 12%

Adjusted EBITDA of $475 million to $525 million

Free Cash Flow Conversion of 50% to 60%

Adjusted EPS of $0.98 – $1.12

Guidance includes anticipated impact from acquisitions or dispositions.

* The Company has excluded a quantitative reconciliation with respect to the Company’s 2026 guidance under the “unreasonable efforts” exception in Item 10(e)(1)(i)(B) of Regulation S-K. See “Non-GAAP Financial Measures” below for additional information.

Stock Repurchase Program

On March 4, 2026, the Board of Directors authorized an extension and a $350.0 million increase in the size of our previously approved stock repurchase program (the “Repurchase Program”). Under the Repurchase Program, as amended, we may repurchase up to an aggregate of $725.0 million of shares of our outstanding Class A common stock, par value $0.001 per share (“Class A Common Stock”), with any previous purchases under the Repurchase Program continuing to count against that limit. With the increase, we have a total of approximately $400.0 million available for repurchases. The Repurchase Program will expire on March 4, 2029.

Video Webcast

Management will host a video webcast on Tuesday, March 10, 2026, at 8:30 a.m. (ET) to discuss results for Stagwell Inc. for the year ended December 31, 2025. The video webcast will be accessible at https://edge.media-server.com/mmc/p/3x58p928/. An investor presentation has been posted on our website at www.stagwellglobal.com and may be referred to during the webcast.

A recording of the webcast will be accessible one hour after the webcast and available for ninety days at www.stagwellglobal.com.

Stagwell Inc.

Stagwell is the challenger network built to transform marketing. We deliver scaled creative performance for the world’s most ambitious brands, connecting culture-moving creativity with leading-edge technology to harmonize the art and science of marketing. Led by entrepreneurs, our specialists in 45+ countries are unified under a single purpose: to drive effectiveness and improve business results for their clients. Join us at www.stagwellglobal.com.

In addition to its reported results, Stagwell Inc. has included in this earnings release certain financial results that the Securities and Exchange Commission (SEC) defines as “non-GAAP Financial Measures.” Management believes that such non-GAAP financial measures, when read in conjunction with the Company’s reported results, can provide useful supplemental information for investors analyzing period to period comparisons of the Company’s results. Such non-GAAP financial measures include the following:

(1) Organic Net Revenue: “Organic net revenue growth” and “Organic net revenue decline” reflects the year-over-year change in the Company’s reported net revenue attributable to the Company’s management of the entities it owns. We calculate organic net revenue growth (decline) by subtracting the net impact of acquisitions (divestitures) and the impact of foreign currency exchange fluctuations from the aggregate year-over-year increase or decrease in the Company’s reported net revenue. The net impact of acquisitions (divestitures) reflects the year-over-year change in the Company’s reported net revenue attributable to the impact of all individual entities that were acquired or divested in the current and prior year. We calculate impact of an acquisition as follows: (a) for an entity acquired during the current year, we present the entity’s current period reported revenue as the impact of the acquisition in the current year; and (b) for an entity acquired in the prior year, we present an amount equal to the entity’s current year net revenue for the same period during which we didn’t own the entity in the prior year as the impact of the acquisition in the current year. We calculate impact of a divestiture as follows: (a) for a divestiture in the current year, we present the entity’s prior year net revenue for the same period during which we no longer owned it in the current year as impact of the divestiture in the current year; and (b) for a divestiture in the prior year, we present the entity’s prior year net revenue for the period during which we owned it in the prior year as impact of the divestiture in the current year. We calculate the impact of any acquisition or divestiture without adjusting for foreign currency exchange fluctuations. The impact of foreign currency exchange fluctuations reflects the year-over-year change in the Company’s reported net revenue attributable to changes in foreign currency exchange rates. We calculate the impact of foreign currency exchange fluctuations for the portion of the reporting period in which we recognized revenue from a foreign entity in both the current year and the prior year. The impact is calculated as the difference between (1) reported prior period net revenue (converted to U.S. dollars at historical foreign currency exchange rates) and (2) prior period net revenue converted to U.S. dollars at current period foreign exchange rates.

(2) Net New Business: Estimate of annualized revenue for new wins less annualized revenue for losses incurred in the period.

(3) Adjusted EBITDA: defined as Net income (loss) attributable to Stagwell Inc. common shareholders excluding non-operating income or expense to achieve operating income (loss), plus depreciation and amortization, stock-based compensation, deferred acquisition consideration adjustments, impairment and other losses, and other items. Other items primarily includes restructuring, certain system implementation, working capital administrative fees and acquisition-related expenses. Adjusted EBITDA for our reportable segments is reconciled to Operating Income (Loss), as Net Income (Loss) is not a relevant reportable segment financial metric.

(4) Adjusted Diluted EPS” is defined as (i) Net income (loss) attributable to Stagwell Inc. common shareholders, plus net income (loss) attributable to Class C shareholders, excluding the impact of amortization expense, impairment and other losses, stock-based compensation, deferred acquisition consideration adjustments, discrete tax items, and other items (as defined above), based on total consolidated amounts, then allocated to Stagwell Inc. common shareholders and Class C shareholders, based on their respective income allocation percentage using a normalized effective income tax rate divided by (ii) the diluted weighted average shares outstanding. The diluted weighted average shares outstanding is calculated as (a) the diluted weighted average number of common shares outstanding plus (b) the shares of Class C Common Stock as if converted to shares of Class A Common Stock if not included because they were anti-dilutive.

(5) Free Cash Flow: defined as Net cash provided from operations less normalized capital expenditures and capitalized software. Free Cash Flow Conversion is the percentage of adjusted EBITDA.

Included in this earnings release are tables reconciling reported Stagwell Inc. results to arrive at certain of these non-GAAP financial measures.

This document contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). The Company’s representatives may also make forward-looking statements orally or in writing from time to time. Statements in this document that are not historical facts, including, statements about the Company’s beliefs and expectations, future financial performance, growth, and future prospects, the Company’s strategy, business and economic trends and growth, technological leadership and differentiation, potential and completed acquisitions, anticipated and actual operating efficiencies and synergies and estimates of amounts for redeemable noncontrolling interests and deferred acquisition consideration, constitute forward-looking statements. Forward-looking statements, which are generally denoted by words such as “ability,” “aim,” “anticipate,” “assume,” “believe,” “better,” “build,” “consider,” “continue,” “could,” “develop,” “drive,” “enhance,” “estimate,” “expect,” “focus,” “forecast,” “future,” “grow,” “guidance,” “improve,” “intend,” “likely,” “maintain,” “may,” “ongoing,”, “outlook,” “plan,” “position,” “possible,” “potential,” “probable,” “project,” “seek,” “should,” “target,” “will,” “would” or the negative of such terms or other variations thereof and terms of similar substance used in connection with any discussion of current plans, estimates and projections are subject to change based on a number of factors, including those outlined in this section.

Forward-looking statements in this document are based on certain key expectations and assumptions made by the Company. Although the management of the Company believes that the expectations and assumptions on which such forward-looking statements are based are reasonable, undue reliance should not be placed on the forward-looking statements because the Company can give no assurance that they will prove to be correct. The material assumptions upon which such forward-looking statements are based include, among others, assumptions with respect to general business, economic and market conditions, the competitive environment, anticipated and unanticipated tax consequences and anticipated and unanticipated costs. These forward-looking statements are based on current plans, estimates and projections, and are subject to change based on a number of factors, including those outlined in this section. These forward-looking statements are subject to various risks and uncertainties, many of which are outside the Company’s control. Therefore, you should not place undue reliance on such statements. Forward-looking statements speak only as of the date they are made, and the Company undertakes no obligation to update publicly any of them in light of new information or future events, if any.

Forward-looking statements involve inherent risks and uncertainties. A number of important factors could cause actual results to differ materially from those contained in any forward-looking statements. Such risk factors include, but are not limited to, the following:

risks associated with international, national and regional unfavorable economic conditions, including the effect of changing tariff and other trade policies, inflation and other macroeconomic factors that could affect the Company or its clients;

demand for the Company’s services, which may precipitate or exacerbate other risks and uncertainties;

inflation and actions taken by central banks to counter inflation;

the Company’s ability to attract new clients and retain existing clients;

the impact of a reduction in client spending and changes in client advertising, marketing and corporate communications requirements;

financial failure of the Company’s clients;

the Company’s ability to retain and attract key employees;

the Company’s ability to compete in the markets in which it operates;

the Company’s ability to achieve its cost saving initiatives;

the Company’s implementation of strategic initiatives;

the Company’s ability to remain in compliance with its debt agreements and the Company’s ability to finance its contingent payment obligations when due and payable, including but not limited to those relating to redeemable noncontrolling interests, deferred acquisition consideration and profit interests;

the Company’s ability to manage its growth effectively;

the Company’s ability to identify and complete acquisitions or other strategic transactions that complement and expand the Company’s business capabilities and successfully integrate newly acquired businesses into the Company’s operations, retain key employees, and realize cost savings, synergies and other related anticipated benefits within the expected time period;

the Company’s ability to identify and complete divestitures and to achieve the anticipated benefits therefrom;

the Company’s ability to develop products incorporating new technologies, including augmented reality, artificial intelligence, and virtual reality, and realize benefits from such products;

the Company’s use of artificial intelligence, including generative artificial intelligence;

adverse tax consequences for the Company, its operations and its stockholders, that may differ from the expectations of the Company, including that recent or future changes in tax laws, potential changes to corporate tax rates in the United States and disagreements with tax authorities on the Company’s determinations that may result in increased tax costs;

adverse tax consequences in connection with the business combination that formed the Company in August 2021, including the incurrence of material Canadian federal income tax (including material “emigration tax”);

the Company’s ability to maintain an effective system of internal control over financial reporting, including the risk that the Company’s internal controls will fail to detect misstatements in its financial statements;

the Company’s ability to accurately forecast its future financial performance and provide accurate guidance;

the Company’s ability to protect client data from security incidents or cyberattacks;

economic disruptions resulting from war and other economic and geopolitical tensions (such as the ongoing military conflicts in Iran and the Middle East, and between Russia and Ukraine), terrorist activities, natural disasters, public health events, and tariff and trade policies;

stock price volatility; and

foreign currency fluctuations.

Investors should carefully consider these risks factors, the additional risk factors outlined under the caption “Risk Factors” in this Form 10-K, and in the Company’s other filings with the Securities and Exchange Commission (the”SEC”) which are accessible on the SEC’s website at www.sec.gov.

SCHEDULE 1 STAGWELL INC. UNAUDITED CONSOLIDATED STATEMENTS OF OPERATIONS (amounts in thousands, except per share amounts)

Three Months Ended December 31,

Year Ended December 31,

2025

2024

2025

2024

Revenue

$

807,444

$

788,708

$

2,909,000

$

2,841,216

Operating Expenses

Cost of services

503,718

502,522

1,845,958

1,842,978

Office and general expenses

203,481

203,887

732,326

711,803

Depreciation and amortization

43,614

38,771

171,249

151,652

Impairment and other losses

–

–

466

1,715

750,813

745,180

2,749,999

2,708,148

Operating Income

56,631

43,528

159,001

133,068

Other income (expenses):

Interest expense, net

(24,431

)

(24,038

)

(96,438

)

(92,317

)

Foreign exchange, net

(1,156

)

645

(1,640

)

(1,656

)

Gain (loss) on sale of business

(2,245

)

–

(2,245

)

–

Bargain purchase gain

9,937

–

9,937

–

Other, net

2,314

(547

)

171

(1,372

)

(15,581

)

(23,940

)

(90,215

)

(95,345

)

Income before income taxes and equity in earnings of non-consolidated affiliates

41,050

19,588

68,786

37,723

Income tax expense

24,321

3,741

38,271

13,182

Income before equity in earnings of non-consolidated affiliates

16,729

15,847

30,515

24,541

Equity in income of non-consolidated affiliates

93

–

111

503

Net income

16,822

15,847

30,626

25,044

Net income attributable to noncontrolling and redeemable noncontrolling interests

(4,162

)

(12,612

)

(1,525

)

(22,785

)

Net income attributable to Stagwell Inc. common shareholders

$

12,660

$

3,235

$

29,101

$

2,259

Earnings Per Common Share:

Basic

$

0.05

$

0.03

$

0.13

$

0.02

Diluted

$

0.05

$

0.03

$

0.08

$

0.02

Weighted Average Number of Common Shares Outstanding:

Basic

251,650

109,266

220,608

110,890

Diluted

258,997

115,147

264,523

115,752

SCHEDULE 2 STAGWELL INC. UNAUDITED COMPONENTS OF NET REVENUE CHANGE (amounts in thousands)

Net Revenue – Components of Change

Change

Three Months Ended December 31, 2024

Foreign Currency

Net Acquisitions (Divestitures)

Organic (1)

Total Change

Three Months Ended December 31, 2025

Organic

Total

Marketing Services

$

240,262

$

2,017

$

1,315

$

1,215

$

4,547

$

244,809

0.5

%

1.9

%

Digital Transformation

84,570

(130

)

5,419

2,335

7,624

92,194

2.8

%

9.0

%

Media & Commerce

161,720

1,745

3,154

11,546

16,445

178,165

7.1

%

10.2

%

Communications

131,736

385

–

(23,796

)

(23,411

)

108,325

(18.1

)%

(17.8

)%

The Marketing Cloud

13,122

485

8,706

5,404

14,595

27,717

41.2

%

111.2

%

Corporate, eliminations and other

(1,787

)

–

–

1,410

1,410

(377

)

(78.9

)%

(78.9

)%

$

629,623

$

4,502

$

18,594

$

(1,886

)

$

21,210

$

650,833

(0.3

)%

3.4

%

(1) See Non-GAAP Financial Measures section above for the definition of Organic Net Revenue.

SCHEDULE 3 STAGWELL INC. UNAUDITED COMPONENTS OF NET REVENUE CHANGE (amounts in thousands)

Net Revenue – Components of Change

Change

Year Ended December 31, 2024

Foreign Currency

Net Acquisitions (Divestitures)

Organic (1)

Total Change

Year Ended December 31, 2025

Organic

Total

Marketing Services

$

905,117

$

3,491

$

9,788

$

41,280

$

54,559

$

959,676

4.6

%

6.0

%

Digital Transformation

324,183

(405

)

13,615

29,779

42,989

367,172

9.2

%

13.3

%

Media & Commerce

601,503

3,396

5,829

(708

)

8,517

610,020

(0.1

)%

1.4

%

Communications

435,626

547

29,002

(71,744

)

(42,195

)

393,431

(16.5

)%

(9.7

)%

The Marketing Cloud

32,265

941

62,229

11,051

74,221

106,486

34.3

%

230.0

%

Corporate, eliminations and other

(2,032

)

–

–

(7,082

)

(7,082

)

(9,114

)

NM

NM

$

2,296,662

$

7,970

$

120,463

$

2,576

$

131,009

$

2,427,671

0.1

%

5.7

%

(1) See Non-GAAP Financial Measures section above for the definition of Organic Net Revenue.

SCHEDULE 4 STAGWELL INC. UNAUDITED SEGMENT OPERATING RESULTS (amounts in thousands)

For the Three Months Ended December 31, 2025

Marketing Services

Digital Transformation

Media & Commerce

Communications

The Marketing Cloud

Corporate, Elimination and Other

Total

Net revenue

$

244,809

$

92,194

$

178,165

$

108,325

$

27,717

$

(377

)

$

650,833

Billable costs

50,555

9,117

32,862

64,037

35

5

156,611

Revenue

295,364

101,311

211,027

172,362

27,752

(372

)

807,444

Billable costs

50,555

9,117

32,862

64,037

35

5

156,611

Staff costs

144,258

63,081

93,713

57,083

14,964

17,055

390,154

Administrative costs

20,304

7,668

25,988

13,799

4,243

12,238

84,240

Unbillable and other costs, net

18,103

154

21,000

2,390

5,511

(1

)

47,157

Adjusted EBITDA(1)

62,144

21,291

37,464

35,053

2,999

(29,669

)

129,282

Stock-based compensation

4,647

1,041

1,127

(435

)

87

3,486

9,953

Depreciation and amortization

12,154

5,924

8,637

6,362

6,078

4,459

43,614

Deferred acquisition consideration

–

4,542

68

(2,143

)

(23

)

–

2,444

Impairment and other losses

–

–

–

–

–

–

–

Other items, net(1)

5,996

366

7,437

1,362

1,042

437

16,640

Operating income (loss)

$

39,347

$

9,418

$

20,195

$

29,907

$

(4,185

)

$

(38,051

)

$

56,631

(1) See Non-GAAP Financial Measures section above for the definition of Adjusted EBITDA and Other items, net.

SCHEDULE 5 STAGWELL INC. UNAUDITED SEGMENT OPERATING RESULTS (amounts in thousands)

For the Year Ended December 31, 2025

Marketing Services

Digital Transformation

Media & Commerce

Communications

The Marketing Cloud

Corporate, Elimination and Other

Total

Net revenue

$

959,676

$

367,172

$

610,020

$

393,431

$

106,486

$

(9,114

)

$

2,427,671

Billable costs

175,145

26,327

80,655

199,146

51

5

481,329

Revenue

1,134,821

393,499

690,675

592,577

106,537

(9,109

)

2,909,000

Billable costs

175,145

26,327

80,655

199,146

51

5

481,329

Staff costs

565,484

247,967

363,031

229,356

68,647

52,411

1,526,896

Administrative costs

105,801

27,267

93,003

50,841

17,613

7,938

302,463

Unbillable and other costs, net

78,333

1,305

64,833

9,300

22,689

(1

)

176,459

Adjusted EBITDA(1)

210,058

90,633

89,153

103,934

(2,463

)

(69,462

)

421,853

Stock-based compensation

19,716

4,122

4,191

6,325

628

19,113

54,095

Depreciation and amortization

52,295

23,174

30,263

25,711

23,514

16,292

171,249

Deferred acquisition consideration

(4,784

)

12,271

3,010

(7,022

)

(10,942

)

–

(7,467

)

Impairment and other losses

–

–

–

222

244

–

466

Other items, net(1)

10,228

1,859

17,549

5,048

3,651

6,174

44,509

Operating income (loss)

$

132,603

$

49,207

$

34,140

$

73,650

$

(19,558

)

$

(111,041

)

$

159,001

(1) See Non-GAAP Financial Measures section above for the definition of Adjusted EBITDA and Other items, net.

SCHEDULE 6 STAGWELL INC. UNAUDITED SEGMENT OPERATING RESULTS (amounts in thousands)

For the Three Months Ended December 31, 2024

Marketing Services

Digital Transformation

Media & Commerce

Communications

The Marketing Cloud

Corporate, Elimination and Other

Total

Net revenue

$

240,262

$

84,570

$

161,720

$

131,736

$

13,122

$

(1,787

)

$

629,623

Billable costs

48,294

2,110

11,719

97,372

–

(410

)

159,085

Revenue

288,556

86,680

173,439

229,108

13,122

(2,197

)

788,708

Billable costs

48,294

2,110

11,719

97,372

–

(410

)

159,085

Staff costs

146,876

60,557

91,108

69,381

10,614

11,685

390,221

Administrative costs

25,300

6,102

22,190

13,646

2,725

3,312

73,275

Unbillable and other costs, net

15,458

605

18,944

2,882

2,860

–

40,749

Adjusted EBITDA(1)

52,628

17,306

29,478

45,827

(3,077

)

(16,784

)

125,378

Stock-based compensation

2,093

(1,480

)

1,866

2,254

157

8,345

13,235

Depreciation and amortization

12,680

5,585

7,301

6,556

3,193

3,456

38,771

Deferred acquisition consideration

3,379

4,221

(1,292

)

9,673

(936

)

–

15,045

Other items, net(1)

8,823

201

1,863

1,403

88

2,421

14,799

Operating income (loss)

$

25,653

$

8,779

$

19,740

$

25,941

$

(5,579

)

$

(31,006

)

$

43,528

(1) See Non-GAAP Financial Measures section above for the definition of Adjusted EBITDA and Other items.

SCHEDULE 7 STAGWELL INC. UNAUDITED SEGMENT OPERATING RESULTS (amounts in thousands)

For the Year Ended December 31, 2024

Marketing Services

Digital Transformation

Media & Commerce

Communications

The Marketing Cloud

Corporate, Elimination and Other

Total

Net revenue

$

905,117

$

324,183

$

601,503

$

435,626

$

32,265

$

(2,032

)

$

2,296,662

Billable costs

172,490

11,473

93,899

267,439

–

(747

)

544,554

Revenue

1,077,607

335,656

695,402

703,065

32,265

(2,779

)

2,841,216

Billable costs

172,490

11,473

93,899

267,439

–

(747

)

544,554

Staff costs

557,776

227,522

356,684

232,096

28,686

46,942

1,449,706

Administrative costs

101,145

21,809

83,572

47,335

9,777

11,408

275,046

Unbillable and other costs, net

70,924

1,393

65,188

10,840

6,117

–

154,462

Adjusted EBITDA(1)

175,272

73,459

96,059

145,355

(12,315

)

(60,382

)

417,448

Stock-based compensation

17,095

6,622

6,265

7,721

805

13,653

52,161

Depreciation and amortization

53,106

22,398

31,450

20,100

12,502

12,096

151,652

Deferred acquisition consideration

5,379

7,911

(7,745

)

18,770

(1,320

)

–

22,995

Impairment and other losses

1,500

–

–

–

–

215

1,715

Other items, net(1)

20,251

3,090

17,103

4,860

629

9,924

55,857

Operating income (loss)

$

77,941

$

33,438

$

48,986

$

93,904

$

(24,931

)

$

(96,270

)

$

133,068

(1) See Non-GAAP Financial Measures section above for the definition of Adjusted EBITDA and Other items, net.

SCHEDULE 8 STAGWELL INC. UNAUDITED RECONCILIATION OF ADJUSTED DILUTED EARNINGS PER SHARE (NON-GAAP MEASURE) (amounts in thousands, except per share amounts)

For the Three Months Ended December 31, 2025

GAAP

Adjustments

Non-GAAP

Net income attributable to Stagwell Inc. common shareholders and adjusted net income

$

12,660

$

64,037

$

76,697

Diluted – Weighted average number of shares outstanding

258,997

–

258,997

Diluted EPS and Adjusted Diluted EPS (1)

$

0.05

$

0.30

Adjustments to Net income

Amortization

$

38,333

Stock-based compensation

9,953

Deferred acquisition consideration

2,444

Other items, net

16,639

67,369

Adjusted tax expense

(3,332

)

$

64,037

(1) See Non-GAAP Financial Measures section above for the definition of Adjusted Diluted EPS.

SCHEDULE 9 STAGWELL INC. UNAUDITED RECONCILIATION OF ADJUSTED DILUTED EARNINGS PER SHARE (NON-GAAP MEASURE) (amounts in thousands, except per share amounts)

For the Year Ended December 31, 2025

GAAP

Adjustments

Non-GAAP

Net income attributable to Stagwell Inc. common shareholders

$

29,101

$

198,129

$

227,230

Net loss attributable to Class C shareholders

(6,637

)

–

(6,637

)

Net income attributable to Stagwell Inc. and Class C shareholders and adjusted net income

$

22,464

$

198,129

$

220,593

Diluted – Weighted average number of common shares outstanding

225,468

–

225,468

Weighted average number of shares of Class C Common Stock outstanding

39,055

–

39,055

Diluted – Weighted average number of shares outstanding

264,523

–

264,523

Diluted EPS and Adjusted Diluted EPS (1)

$

0.08

$

0.83

Adjustments to Net Income

Amortization

$

145,506

Impairment and other losses

466

Stock-based compensation

54,095

Deferred acquisition consideration

(7,467

)

Other items, net

46,792

239,392

Adjusted tax expense

(41,263

)

$

198,129

(1) See Non-GAAP Financial Measures section above for the definition of Adjusted Diluted EPS.

SCHEDULE 10 STAGWELL INC. UNAUDITED RECONCILIATION OF ADJUSTED DILUTED EARNINGS PER SHARE (NON-GAAP MEASURE) (amounts in thousands, except per share amounts)

For the Three Months Ended December 31, 2024

GAAP

Adjustments

Non-GAAP

Net income attributable to Stagwell Inc. common shareholders

$

3,235

$

22,778

$

26,013

Net income attributable to Class C shareholders

–

41,549

41,549

Net income attributable to Stagwell Inc. and Class C and adjusted net income

$

3,235

$

64,327

$

67,562

Diluted – Weighted average number of common shares outstanding

115,147

–

115,147

Weighted average number of shares of Class C Common Stock outstanding

–

151,649

151,649

Diluted – Weighted average number of shares outstanding

115,147

151,649

266,796

Diluted EPS and Adjusted Diluted EPS (1)

$

0.03

$

0.25

Adjustments to Net income

Amortization

$

30,572

Stock-based compensation

13,235

Deferred acquisition consideration

15,045

Other items, net

14,799

73,651

Adjusted tax expense

(20,618

)

53,033

Net income attributable to Class C shareholders

11,294

$

64,327

Allocation of adjustments to Net income

Net income attributable to Stagwell Inc. common shareholders

$

22,778

Net income attributable to Class C shareholders – add-backs

30,255

Net income attributable to Class C shareholders

11,294

41,549

$

64,327

(1) See Non-GAAP Financial Measures section above for the definition of Adjusted Diluted EPS.

SCHEDULE 11 STAGWELL INC. UNAUDITED RECONCILIATION OF ADJUSTED DILUTED EARNINGS PER SHARE (NON-GAAP MEASURE) (amounts in thousands, except per share amounts)

For the Year Ended December 31, 2024

GAAP

Adjustments

Non-GAAP

Net income attributable to Stagwell Inc. common shareholders

$

2,259

$

82,506

$

84,765

Net income attributable to Class C shareholders

–

126,735

126,735

Net income attributable to Stagwell Inc. and Class C shareholders and adjusted net income

$

2,259

$

209,241

$

211,500

Diluted – Weighted average number of common shares outstanding

115,752

–

115,752

Weighted average number of shares of Class C Common Stock outstanding

–

151,649

151,649

Diluted – Weighted average number of shares outstanding

115,752

151,649

267,401

Diluted EPS and Adjusted Diluted EPS (1)

$

0.02

$

0.79

Adjustments to Net income

Amortization

$

122,442

Impairment and other losses

1,715

Stock-based compensation

52,161

Deferred acquisition consideration

22,995

Other items, net

55,857

255,170

Adjusted tax expense

(63,073

)

192,097

Net income attributable to Class C shareholders

17,144

$

209,241

Allocation of adjustments to Net income

Net income attributable to Stagwell Inc. common shareholders

$

82,506

Net income attributable to Class C shareholders – add-backs

109,591

Net income attributable to Class C shareholders

17,144

126,735

$

209,241

(1) See Non-GAAP Financial Measures section above for the definition of Adjusted Diluted EPS.

SCHEDULE 12 STAGWELL INC. UNAUDITED CONSOLIDATED BALANCE SHEETS (amounts in thousands)

December 31, 2025

December 31, 2024

ASSETS

Current Assets

Cash and cash equivalents

$

104,537

$

131,339

Accounts receivable, net

735,752

716,415

Expenditures billable to clients

164,694

173,194

Other current assets

157,309

114,200

Total Current Assets

1,162,292

1,135,148

Fixed assets, net

73,081

72,706

Right-of-use assets – operating leases

213,576

219,400

Goodwill

1,595,238

1,554,146

Other intangible assets, net

834,248

836,783

Deferred tax assets

281,057

46,926

Other assets

55,055

43,112

Total Assets

$

4,214,547

$

3,908,221

LIABILITIES, REDEEMABLE NONCONTROLLING INTERESTS (“RNCI”), AND SHAREHOLDERS’ EQUITY

Current Liabilities

Accounts payable

$

548,320

$

449,347

Accrued media

239,490

245,883

Accruals and other liabilities

291,554

265,356

Advance billings

329,815

294,609

Current portion of lease liabilities – operating leases

55,386

60,195

Current portion of deferred acquisition consideration

15,446

51,906

Total Current Liabilities

1,480,011

1,367,296

Long-term debt

1,326,013

1,353,624

Long-term portion of deferred acquisition consideration

24,598

50,209

Long-term lease liabilities – operating leases

224,397

245,397

Deferred tax liabilities

54,726

47,239

Long-term tax receivable agreement liability

252,390

25,493

Other liabilities

51,077

33,646

Total Liabilities

3,413,212

3,122,904

Redeemable Noncontrolling Interests

24,968

8,412

Commitments, Contingencies and Guarantees

Shareholders’ Equity

Common shares – Class A

252

115

Common shares – Class C

–

2

Paid-in capital

744,463

343,647

Retained earnings

32,930

11,740

Accumulated other comprehensive loss

(19,252

)

(23,773

)

Stagwell Inc. Shareholders’ Equity

758,393

331,731

Noncontrolling interests

17,974

445,174

Total Shareholders’ Equity

776,367

776,905

Total Liabilities, Redeemable Noncontrolling Interests and Shareholders’ Equity

$

4,214,547

$

3,908,221

SCHEDULE 13 STAGWELL INC. UNAUDITED SUMMARY CASH FLOW DATA (amounts in thousands)

Years Ended December 31,

2025

2024

Cash flows from operating activities:

Net income

$

30,626

$

25,044

Adjustments to reconcile net income to cash provided by operating activities:

Stock-based compensation

54,095

52,161

Depreciation and amortization

171,249

151,652

Amortization of right-of-use lease assets and lease liability interest

67,495

75,117

Impairment and other (gains) losses

(3,116

)

1,715

Deferred income taxes

10,439

(10,686

)

Adjustment to deferred acquisition consideration

(7,467

)

23,005

Loss (gain) on sale of business

2,245

–

Bargain purchase gain

(9,937

)

–

Other, net

7,519

7,622

Changes in working capital:

Accounts receivable

28,787

8,465

Expenditures billable to clients

12,012

(54,350

)

Other current assets

(51,534

)

(6,200

)

Accounts payable

73,573

24,438

Accrued expenses and other liabilities

(42,244

)

(28,658

)

Advance billings

25,574

(22,651

)

Current portion of lease liabilities – operating leases

(76,465

)

(83,905

)

Deferred acquisition related payments

(1,823

)

(19,910

)

Net cash provided by operating activities

291,028

142,859

Cash flows from investing activities:

Capitalized software

(67,489

)

(35,094

)

Capital expenditures

(43,741

)

(18,912

)

Acquisitions, net of cash acquired

(6,179

)

(103,254

)

Proceeds from sale of business, net

10,850

–

Other

(7,119

)

(5,212

)

Net cash used in investing activities

(113,678

)

(162,472

)

Cash flows from financing activities:

Repayment of borrowings under revolving credit facility

(2,026,000

)

(1,755,000

)

Proceeds from borrowings under revolving credit facility

1,999,326

1,960,000

Shares repurchased and cancelled

(134,261

)

(108,249

)

Distributions to noncontrolling interests

(9,662

)

(26,723

)

Payment of deferred consideration

(33,343

)

(29,774

)

Purchase of noncontrolling interest

–

(3,316

)

Debt financing and other costs

(6,077

)

–

Net cash (used in) provided by financing activities

(210,017

)

36,938

Effect of exchange rate changes on cash and cash equivalents

5,865

(5,723

)

Net increase (decrease) in cash and cash equivalents

ORLANDO, FLORIDA / ACCESS Newswire / March 9, 2026 / Unusual Machines (NYSE American:UMAC) (“Unusual Machines” or the “Company”), a leading provider of NDAA-compliant drone components, today announced its financial results for the fourth quarter and fiscal year ended December 31, 2025 and is anticipating filing its Form 10-K with the U.S. Securities and Exchange Commission for the fiscal year ended December 31, 2025 in the coming days. The Company provided the following letter to its shareholders from CEO Allan Evans.

Dear Shareholders,

This shareholder letter follows the completion of our fourth quarter and fiscal year ended December 31, 2025.

2025 represented a turning point for Unusual Machines. During the year we financed and then rapidly expanded our operations. We executed against our strategy to build an enterprise sales business and have emerged as a leading domestic supplier of NDAA-compliant drone components.

During the year we strengthened the financial position of the company to execute an aggressive expansion through multiple financings. As of December 31, 2025, we held approximately $103 million in cash and $39 million in short-term investments, with no debt, resulting in net working capital of approximately $157 million. This capital position allows us to continue scaling manufacturing capacity, expanding our workforce, and investing in the infrastructure required to support the rapidly growing domestic drone ecosystem.

The growth in operations is now being realized in revenue increases. Revenue for 2025 totaled approximately $11.2 million, representing 101% year-over-year growth, and fourth quarter revenue was approximately $4.9 million, representing 133% sequential quarterly growth. This rapid growth reflects our operational scaling along with increasing demand for our products from enterprise customers.

We want to take this opportunity to provide additional context around our operational progress, financial results, and the scaling of Unusual Machines as we position the company for the next stage of growth.

Operations Update

Operationally, 2025 is a tale of two halves. The first half of the year was preparation and resourcing for growth while the second half of the year was the start of rapid operational expansion. Unusual Machines started to scale rapidly in the second half of 2025 as enterprise demand for NDAA-compliant drone components rapidly increased.

Hardware businesses like Unusual Machines must expand operational capacity substantially before revenue growth is realized. This suggests that headcount expansion is the earliest indicator of scaling and revenue improvements should come about a quarter later. In other words, we need to scale engineering, manufacturing, and operational staff to support product development and production and not realize the revenue until after the products are made and shipped.

Our workforce expansion started in the third quarter. Headcount grew from 19 employees at the end of the second quarter of 2025 to 38 employees at the end of the third quarter, and 81 employees by the end of the fourth quarter. As of today, the company has grown to more than 140 employees, and we are continuing to expand and scale production.

Revenue expansion roughly trailed operational expansion by a quarter. Revenue for quarter 2 was approximately $2.1 million, quarter 3 was approximately $2.1 million and quarter 4 was approximately $4.9 million. The capacity in quarter 3 can be approximated as double the capacity in quarter 2 (headcount doubled from 19 to 38). This quarter 3 capacity expansion is the driving force behind the quarter 4 revenue growth.

There are many other growth drivers that were initiated in the second half. We have expanded our footprint from 6,900 sq ft to 62,500 sq ft across 5 locations in Orlando. We began U.S. production of motors in November and Fat Shark headsets in January of 2026. Transitioned to a 25,000 sq ft fulfillment center in December and continue to add new employees to each operations center to meet rapidly scaling demand.

Cash Flow Management

Responsible cash management has always been core to our ethos, and I want to highlight how we balance the costs of operational growth with our cash management strategy.

We ended the year with approximately $103.3 million in cash, compared to approximately $3.7 million at the end of 2024. The increase in cash was primarily driven by several equity financings completed during the year as well as warrant exercises and ATM activity. Over the course of 2025 we raised $157.8 million through equity sales. These financings allow us to invest aggressively in scaling the company while maintaining financial flexibility and providing a working capital basis for us to manage inventory and material flow.

Cash can be allocated to many different balance sheet categories at any given time. It can be used to purchase inventory, fund capital equipment, etc. The purpose of these balance sheet activities is to use the cash to generate a positive return. The best way to measure cash flow for our business is to aggregate these categories and subtract out payables to quickly understand our entire business. We call this our working capital and is summarized in Table 3. At the end of 2025, our working capital was approximately $157.4 million. Our working capital at the end of 2024 was $5.2 million and across 2025 we raised $157.8 million through equity sales. Through all activities across 2025 we generated a cash loss of approximately $5.6 million.

In this same year, we recognized a GAAP net loss of approximately $19.2 million. This GAAP loss is primarily driven by non-cash stock compensation expense of approximately $15.7 million. Reference Table 2 for additional details on our net loss to operational loss for the fourth quarter. I believe that if Unusual Machines was cash flow positive with a relatively minimal operational net loss we would be in the “goldilocks” zone for rapid growth. It demonstrates that we are constantly re-investing in maximum growth while not creating risks from significant cash depletion. As long as we continue to sustain high YoY growth rates, we will target this type of financial performance.

Looking Ahead

Our priorities moving forward remain clear.

Scale Manufacturing

We are continuing to scale as quickly as possible. In 2026 we have already added a second and third shift to our motor production, added a second shift to our flexible assembly building, and started Fat Shark headset production. We anticipate adding battery pack manufacturing in 2026 and camera manufacturing in late 2026. We plan to dramatically increase our motor production capacity in the second half of 2026 with our automated production equipment.

Grow Revenue and Manage Margins

As we scale manufacturing, we will need to grow revenues to consume the material or we run the risk of scaling past demand and incurring significant losses. We do not believe we will be demand limited in the next 18 months. The Drone Dominance program (www.dronedominance.io) indicates the need for U.S. production of 90,000 drones in 2026 and 250,000 drones in 2027. Each drone represents about $1,000 in total revenue potential for Unusual Machines. This provides an immediately addressable market of at least $90 million this year and $250 million next year without considering the market potential of any of the other government and commercial drone programs.

Introducing new products, processes, and production facilities results in initial inefficiencies that will reduce gross margins in the short term. This margin impact is generally the most pronounced in the quarter after the facility is operational. For instance, our gross margins in Q4 of 2025 were approximately 36% while our margins from just motor production were approximately 20%. We expect margins from motor production will dip further in Q1 before rebounding as the margin impacts are not realized until after the product is shipped. Once we get past these initial inefficiencies, we will work to return margins to our 40% target.

Drive Toward Cash Flow Positive Operations

We were not cash flow positive as a company in 2025 and our operations realized a loss. Our long-term goal is to build a profitable and sustainable business. The next step toward this is for our operations to become cash flow positive. We are pushing to achieve this by the end of 2026 as revenues increase and margins recover from the anticipated drop due to the inefficiencies that come from the introduction of new operating centers and processes.

Closing Thoughts

In 2025 Unusual Machines finalized the transformation from a retail channel to a domestic drone component producer and initiated growth. The progress made in the second half of 2025 gives us a leadership position as we pursue the emerging market opportunity created by the Department of War and the FCC regulatory actions emphasizing the need for a domestic supply chain.